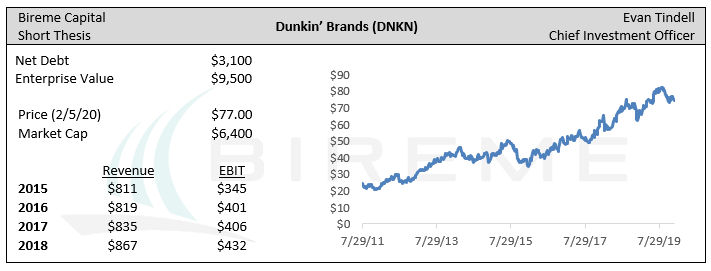

|

In Q1, FV had its worst result ever, down -26.4% net of fees. It is of little solace that the broader market was down as well, with the S&P 500 falling -19.4%.

In our last letter, I tried to convey a sense of urgency while remaining calm and hopeful during this difficult time. However, I have found that sustaining that positive mental state is easier said than done for me personally. Some clients have told me they are struggling as well. Below are some thoughts I wrote for them on maintaining equanimity and hope, both for their investment portfolio and for their health. I hope it is valuable.

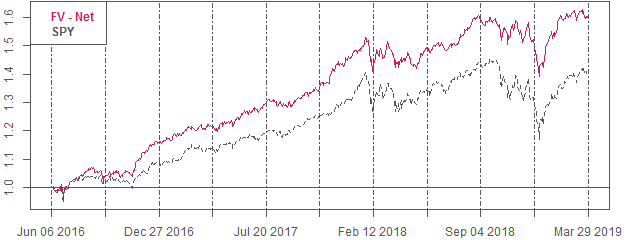

We sent out our last letter only two weeks ago on February 27th, warning that although the market had fallen -12% in a week, valuations were still high, and signs of speculative excess and deteriorating fundamentals were legion. Fundamental Value returned 8.3% for the fourth quarter, slightly trailing the market’s return of 9.0%. For the year, FV was up 29.7% vs the S&P 500’s 31.2% return. Since inception in 2016, FV has beaten the market by 4.4% annualized after fees, returning 19.2% annualized.1 Bireme Capital LLC is an SEC Registered Investment Advisor. Registration does not constitute an endorsement of the firm nor does it indicate that the advisor has attained a particular level of skill or ability. This piece is for informational purposes only. If not specified, quarter end values are used to calculate returns. While Bireme believes the sources of its information to be reliable, it makes no assurances to that effect. Bireme is also under no obligation to update this post should circumstances change. Nothing in this post should be construed as investment advice, and it is not an offer to sell or buy any security. Bireme clients may (and usually do) have positions in the securities mentioned.  THE LOW-VOLATILITY ANAMOLY For most of its existence (Jan 2010 to today), the S&P Low Volatility Index (SP5LVI Index on Bloomberg) traded in line with the S&P 500 on a valuation basis. However, investor interest in these stocks has grown materially, likely due to academic research showing the outperformance of stocks whose prices varied less than the market. This interest has meant asset growth for ETFs that employ a low-volatility strategy. For example, AUM for the iShares US Minimum Volatility ETF, USMV, has skyrocketed, up about 15x in the last five years.  Unsurprisingly, the surge in assets thrown at low-vol has resulted in higher valuations, and these stocks now trade at >25x earnings vs 22x for the S&P 500.

Fundamental Value slightly outperformed in Q3, returning 2.0% after fees vs 1.8% for the S&P 500. This brings the strategy’s annualized return to 17.9% vs 13.1% for the broader market. The second quarter of 2019 saw positive returns across nearly the entire Fundamental Value portfolio, with the strategy up 5.3% after fees relative to the S&P 500 at 4.2%. One of our favorite current holdings, Bollore SA, is a conglomerate that we think trades at a large discount to fundamental value. Bollore has an underappreciated and rapidly growing asset in music label Universal Music Group though Bollore's stake in Vivendi. Bollore also offers a large discount at the corporate level driven by availability bias, a bias that causes shareholders to focus on the most available information – in this case, the reported share count. The first quarter of 2019 was one of Fundamental Value's largest gains since inception, returning 11.5% net versus a gain of 13.5% for the S&P 500. For the S&P, this was merely a reversal of losses created in the fourth quarter, when the market dropped -13.5%. Since FV only dropped -9.4% in Q4, we've come out 2.9% ahead during this 6 month period.

Investor biases

A core belief of ours at Bireme Capital is that human cognitive biases drive security mispricings. This is not to say that we don’t believe in mostly-efficient markets, or that we are unaware that investor biases often cancel each other out. We simply believe that, occasionally, biased investors bunch together on a single side of the ledger, resulting in a mispriced stock. |